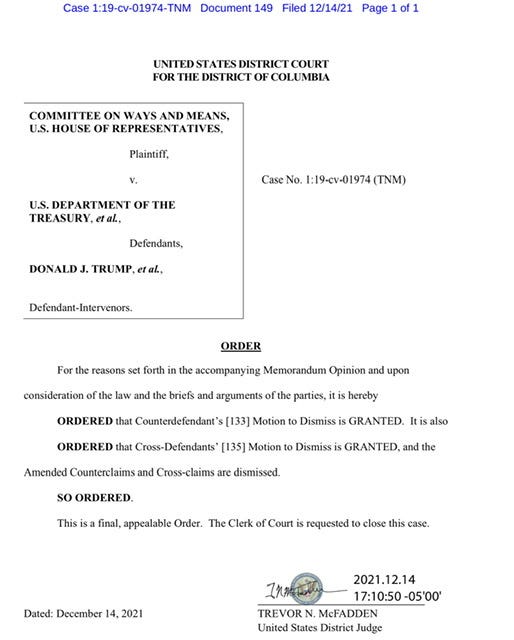

MEMORANDUM OPINION (see DDC-ECF) re Counterdefendant's 133 Motion to Dismiss and Cross-Defendants' 135 Motion to Dismiss. Signed by Judge Trevor N. McFadden on 12/14/21

In Judge Trevor McFadden’s 45 page Memorandum/Opinion (remember that this Judge was a Trump appointee) the Court ruled that Trump and that Congress is due “great deference” coupled with the power our Constitution vest with them as a co-equal branch of Government. Specifically citing that Congress’ has robust powers in its line of inquiries, specifically as it relates to a Legislative purpose.:

“Even the special solicitude accorded former Presidents does not alter the outcome,”

“[Trump] is wrong on the law” …requires audits of the sitting President, is a subterfuge for improper motive…”

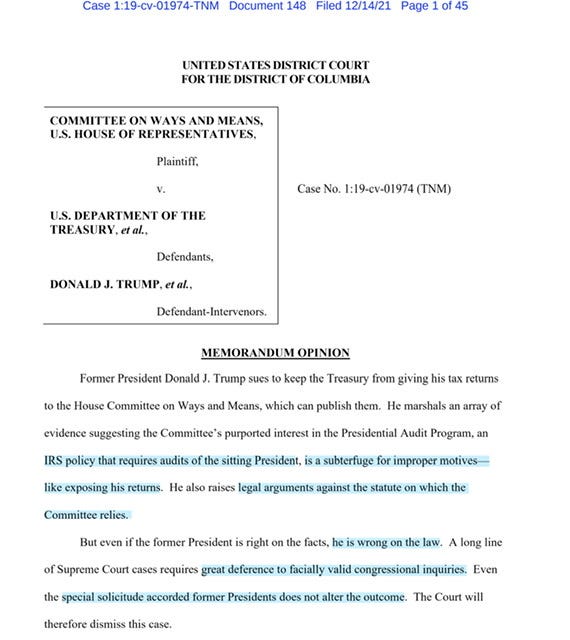

Trump sues to keep the Treasury from giving his tax returns to the House Committee on Ways and Means, which can publish them. He marshals an array of evidence suggesting the Committee’s purported interest in the Presidential Audit Program, an IRS policy that requires audits of the sitting President, is a subterfuge for improper motives—like exposing his returns. He also raises legal arguments against the statute on which the Committee relies.

But even if the former President is right on the facts, he is wrong on the law. A long line of Supreme Court cases requires great deference to facially valid congressional inquiries. Even the special solicitude accorded former Presidents does not alter the outcome

Underlying documents cited in today’s Memorandum/Opinion cites a

2000 Treasury Report, which you can read in its entirety here and that will help you fully understand pages 2 thru 16 of today’s Order/Memorandum/Opinion

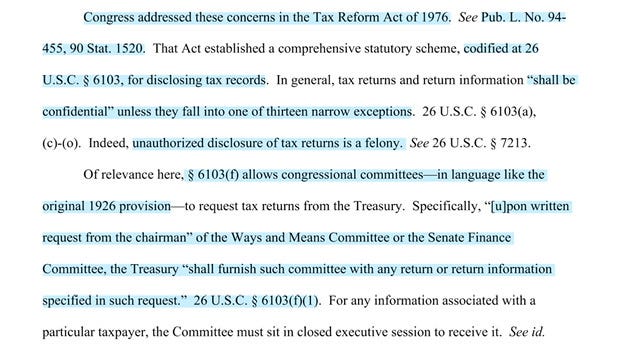

Pub. L. No. 94-455, 90 Stat. 1520 -regarding the Nixon Administration and specifically President Nixon improperly accessing Tax Returns of his perceived political enemies

After President Nixon - Congress enacted and codified certain procedures as to safeguard the public disclosure of tax return and later codified 26 U.S.C. § 6103(f)(1)

As noted on page 3:

…§ 6103(f) allows congressional committees—in language like the original 1926 provision—to request tax returns from the Treasury. Specifically, “[u]pon written request from the chairman” of the Ways and Means Committee or the Senate Finance Committee, the Treasury “shall furnish such committee with any return or return information specified in such request.” 26 U.S.C. § 6103(f)(1). For any information associated with a particular taxpayer, the Committee must sit in closed executive session to receive it…

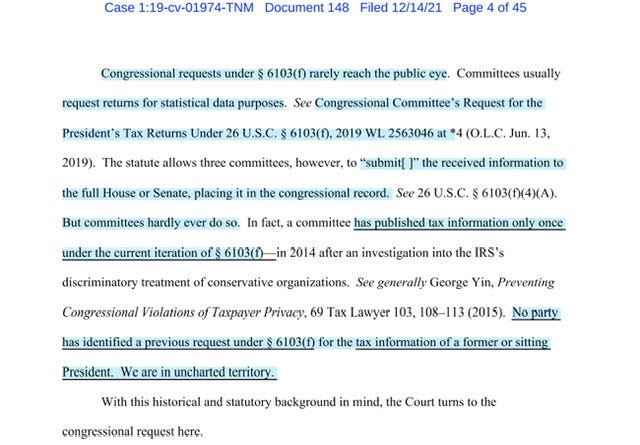

The Court only found ONE instance where Congress published a tax return…

The subtext here (and if you’ll recall those long forgotten twitter threads) that Trump’s specious argument that Congress would publish his tax returns -the Court rejected Trump’s specious and conclusory arguments that some how members of Congress would commit a felony by unlawfully publishing Trump’s taxes:

More broadly the Court opined that Trump’s argument lacked sufficient case law to support his assertion that the “radical democrats will publish my taxes as part of the ongoing witch hunt” remember that in Trump’s deluded mind he is the perennial victim

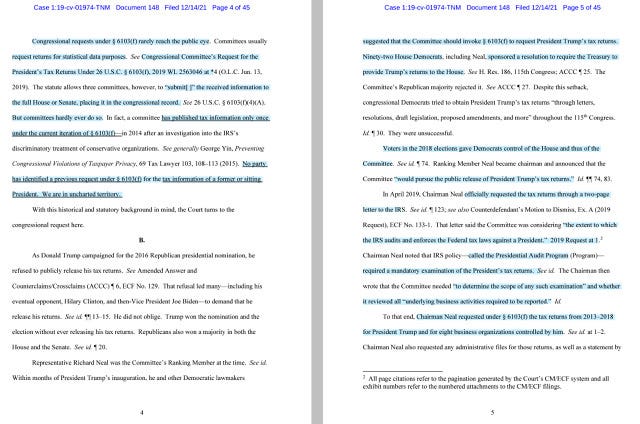

Voters in the 2018 elections gave Democrats control of the House and thus of the Committee. See id. ¶ 74. Ranking Member Neal became chairman and announced that the Committee “would pursue the public release of President Trump’s tax returns.” Id. ¶¶ 74, 83.

In April 2019, Chairman Neal officially requested the tax returns through a two-page letter to the IRS.

Steve Mnuchin aided and abetted Donald Trump’s request to shield his tax returns…

Also see June 2021 DOJ-OLC Memo-Slip Opinion - because (you do get yet another federal judge noted that Trump lost the 2020 General Election], right) under the Biden Administration DOJ -the OLC published a revised slip opinion there were no new set of facts. The June 2021 OLC slip opinion was made on the same subset of facts and documents that the Trump-DOJ’s 2019 Slip Opinion.

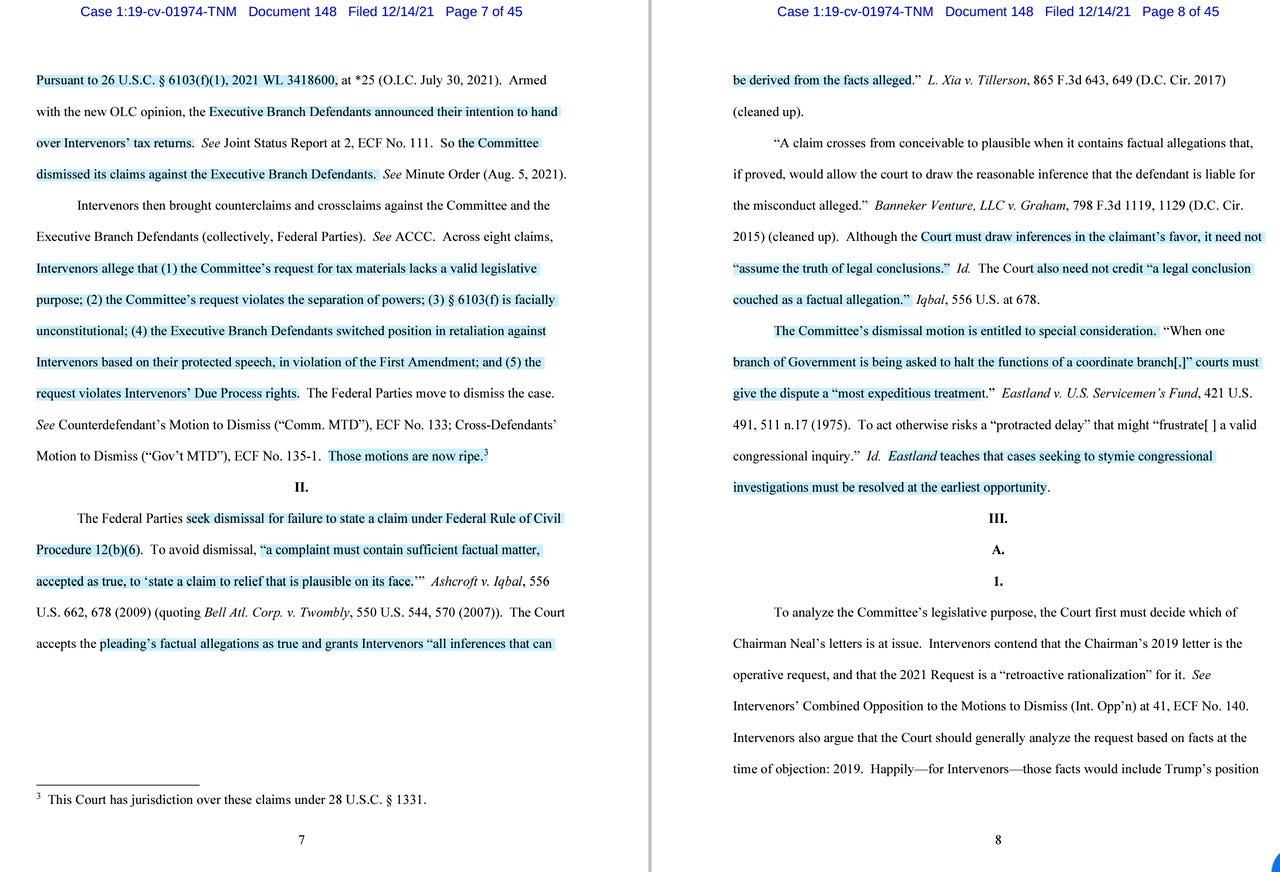

..dismissal for failure to state a claim under Federal Rule of Civil Procedure 12(b)(6)..

Furthermore the Court properly discussed that Trump’s lawsuit was an overt attempt to further delay and frustrate Congress by unlawfully withholding Trump’s tax returns from the House Ways and Means Committee…

The Treasury denied his request. Reviewing public statements by congressional Democrats, the Treasury concluded that the request’s stated purpose contradicted what Democrats had “repeatedly said was the request’s intent: to publicly release the President’s tax returns.” ACCC ¶ 217. The Department of Justice agreed. In a memorandum opinion, DOJ’s Office of Legal Counsel (OLC) summarized public statements from Democrats and found that no one had previously explained an interest in the tax returns by reference to the IRS audit Program. See id. ¶ 219–20. The Committee’s newly asserted rationale “blink[ed] reality” and was “pretextual.” Id. ¶ 220.

…The Federal Parties seek dismissal for failure to state a claim under Federal Rule of Civil Procedure 12(b)(6). To avoid dismissal, “a complaint must contain sufficient factual matter, accepted as true, to ‘state a claim to relief that is plausible on its face.’…be derived from the facts alleged.” L. Xia v. Tillerson, 865 F.3d 643, 649 (D.C. Cir. 2017)

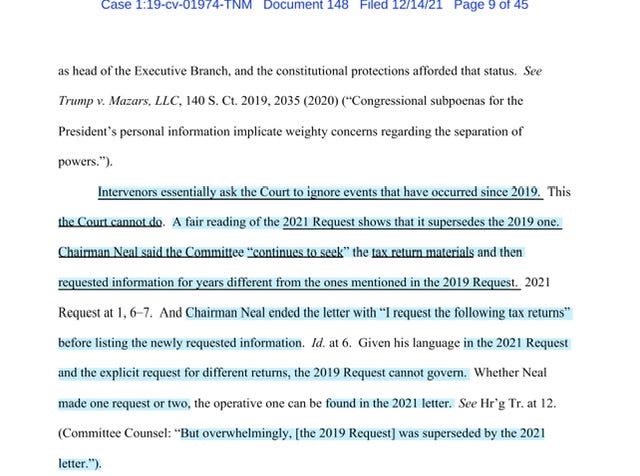

BRUTAL -just brutal - the 2019 Request cannot govern.

Intervenors essentially ask the Court to ignore events that have occurred since 2019. This the Court cannot do. A fair reading of the 2021 Request shows that it supersedes the 2019 one. Chairman Neal said the Committee “continues to seek” the tax return materials and then requested information for years different from the ones mentioned in the 2019 Request. 2021 Request at 1, 6–7.

…Chairman Neal ended the letter with “I request the following tax returns” before listing the newly requested information. Id. at 6. Given his language in the 2021 Request and the explicit request for different returns, the 2019 Request cannot govern. Whether Nealmade one request or two, the operative one can be found in the 2021 letter.Intervenors essentially ask the Court to ignore events that have occurred since 2019. This the Court cannot do. A fair reading of the 2021 Request shows that it supersedes the 2019 one. …Given his language in the 2021 Request and the explicit request for different returns, the 2019 Request cannot govern. Whether Neal made one request or two, the operative one can be found in the 2021 letter.

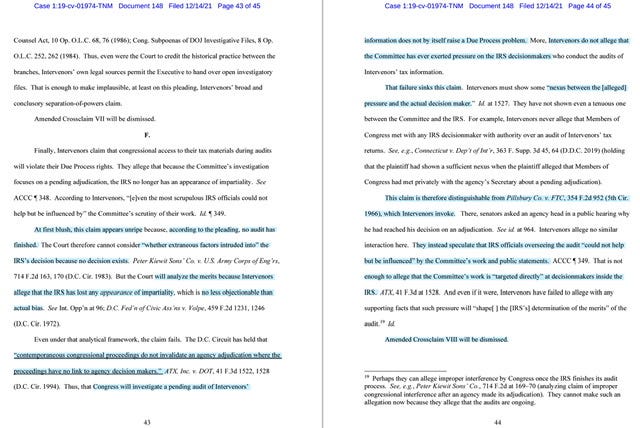

Again you can read the full 45 page Memorandum/Opinion via this DDC-ECF link or you can pull it down from my Scribd Account but pages 43 et seq really drives home the point that Trump’s arguments are not moored from the facts, the codified language and the criminally of unlawfully publishing Trump’s tax returns -hence conclusory arguments are not the best argument because the court obliterated Trump’s allegations. Again the recently docketed Memorandum can be pulled down from:

Right now I just don’t have the bandwidth to do a deeper or more detailed article. But I felt that my readers should have access to today’s Memorandum. Also note that Trump has 14 days to appeal today’s ruling. And naturally Mr Vexatious Litigant will likely file a notice of appeal. This was never about members of Congress unlawfully publishing Trump taxes -this is all about Trump’s Triple-D litigation strategy. So to those who falsely claimed I was wrong, I accept your apology (snort). Also here’s your daily dose of saltwater therapy it’s only Tuesday and I’m operating on less than 3 hours sleep and I’m main-lining Red Bull because my work day isn’t over and I will likely walk into my house after midnight only to turn around and leave by 5AM -so you’ll have to forgive my brevity -or not.

Thank you for this!!! The moment of absolute zen and the courts docs of denial. I can't believe he actually tried to use "the witch hunt" for a reason. Can he appeal to a higher court?

I do forgive any brevity, in light of your superb dedication. Thanks for letting is see what transpired. 14 days is too long.

Thank you for this!!! The moment of absolute zen and the courts docs of denial. I can't believe he actually tried to use "the witch hunt" for a reason. Can he appeal to a higher court?